Strategic report

1. Objectives and operating environment

The directors present their strategic report for the year ended 31 March 2020.

PSAA’s responsibilities derive from the provisions of the Local Audit and Accountability Act 2014 and the Local Audit (Appointing Person) Regulations 2015 made under that Act. The company is specified as an appointing person for principal local government bodies, including local police bodies. These responsibilities became operational from 1 April 2018 and are the focus of the company’s purpose from that date. PSAA’s responsibilities and aims are expressed through a series of objectives, covering:

- appointing auditors to relevant authorities;

- consulting on and setting a scale or scales of fees, and charging fees, for the audit of accounts of relevant authorities;

- ensuring that public money from audit fees continues to be accounted for properly and is protected;

- overseeing the delivery of consistent, high quality and effective audit services to relevant authorities;

- ensuring effective management of contracts with firms for audit services to relevant authorities;

- being financially responsible having regard to the efficiency of operating costs and transparently safeguarding fees charged to audited bodies; and

- leading its people as a good employer.

A memorandum of understanding with the Ministry of Housing, Communities and Local Government sets out the broad framework in which PSAA operates. The memorandum contains the agreed principles regarding PSAA’s operation and the mechanisms for its accountability for, and safeguarding of, public money in the form of audit fees charged to audited bodies.

The PSAA Board believes that strong corporate governance supports the future long-term success of PSAA and has established a comprehensive governance framework to support its functions as an appointing person. The Board takes very seriously its duty under Section 172 of the Companies Act 2006 to promote the success of the company. The Act states that ’A director of a company must act in the way he considers, in good faith, would be most likely to promote the success of the company for the benefit of its members as a whole, and in doing so have regard (amongst other matters) to:

- the likely consequences of any decision in the long term;

- the interests of the company’s employees;

- the need to foster the company’s business relationships with suppliers, customers and others;

- the impact of the company’s operations on the community and the environment; and

- the desirability of the company maintaining a reputation for high standards of business conduct.’

PSAA is wholly owned by the Improvement and Development Agency (IDeA). IDeA is the company’s sole member. As founder of the company IDeA’s role is to support PSAA in discharging its functions and achieving its objectives. The IDeA acknowledges the independence of the company and the responsibility for running the company as that of PSAA and the Board. The Board has satisfied itself that consideration of the requirements of Section 172, and the directors’ duties under it, have informed and guided the Board’s work in the past year.

The following explains how we consider we have had regard to promoting the success of the company in relation to each of the specific requirements of Section 172.

(a) The likely consequences of any decision in the long term

The Board considers how to promote the long-term success of the organisation on a continuous basis, providing effective leadership and oversight of PSAA as it seeks to achieve its objectives. Its decision making is influenced by active consideration of PSAA’s position, role and relationships within the new local audit system as a whole. The Board is mindful of the fact that PSAA’s success depends to a large extent upon the ability of the larger system to deliver for and meet the needs of audited bodies and users of audited accounts. To achieve this, PSAA meets and works closely with other key players in the local audit system seeking to influence decisions for improvement of the system overall.

The Sir Tony Redmond review, commissioned by the Government, is expected to make recommendations for the improvement and strengthening of the local audit system. It is therefore of great interest to PSAA. The company has endeavored to assist and support the review and provided information, evidence and explanations to the review team throughout its work. Reports derived from research projects have also been shared.

Our 5 year Medium Term Financial Plan (MTFP) reflects a healthy financial position. PSAA operates on a not-for-profit basis. From time to time the Board approves the distribution of surplus funds to audited bodies after ensuring PSAA has sufficient funds to pay for its operating expenses and manage its cash flow. A distribution of £3.5m in respect of the transitional period was made in December 2019. The transitional arrangements (2015-2018) and current appointing person arrangements are accounted for separately in the MTFP. The Board reviews the company’s financial position at every Board meeting, including the most up-to-date forecast. We approve our annual accounts following detailed scrutiny by and a recommendation to do so from the audit committee. Our treasury management policy is also reviewed annually by the audit committee which makes recommendations to the Board as appropriate.

As a Board we are responsible for overseeing the company’s arrangements for risk management, identifying key risks, considering risk appetite, and agreeing appropriate mitigation strategies. More detail on our risk management processes is included in Section 3 of the Strategic Report.

All decisions are taken with due regard to the company’s purpose and objectives (as set out in the Articles of Association and other relevant documents), the effective and efficient use of public funds and the need to ensure delivery of high quality and cost-effective audit services.

(b) The interests of the company’s employees

We aim to be a good employer, encouraging a culture of openness and transparency, developing people to the best of their abilities and offering competitive remuneration and benefits to recruit and retain staff. The Board recognises that our small team of well qualified staff are critical to the success of PSAA.

We completed a significant staff restructuring exercise in 2018/19, to align the number and skills of staff with our business needs in the context of the company’s new responsibilities as an appointing person. The restructuring reduced the number of staff to six, establishing a team which has the right skills and experience for the company’s new role, and contributing to savings of £370,000 per annum (39%) in our cost base. The Board monitors the organisational work streams and capacity via regular updates from the Chief Executive. Given the challenges faced by the company and the local audit system more widely during the year, which has generated a significant amount of additional work, the Board has recognised the need to enhance the existing structure with additional resource and skills. This has been achieved through three fixed term contracts. This provides a flexible model which can be reviewed in light of skills and capacity requirements as circumstances change. We will continue to monitor the pay and benefits package with reference to market rates and company requirements.

We are committed to developing our staff and enabling them to realise their potential. During 2019/20 the focus has been on bedding in the new structure and developing the team in their new roles. To this end, all staff attended an away day aimed at developing team working and setting out the vision for the company as it evolved into an ‘appointing person’. Personal Development Plans are being put in place to support individual staff needs as appropriate. Employees have access to the LGA e-learning platform in order to receive regular training on a variety of topics including annual mandatory refreshed training on IT security and information governance.

During the year, PSAA’s suite of HR policies were reviewed to ensure that they were appropriate for a small organisation and suitable for the culture of the company going forward. All staff were consulted on the changes as part of the development process.

With a small team, good communication is imperative. Board and audit committee papers are accessible to all staff. All employees are kept up to date with items considered at Board meetings and in relation to PSAA’s finances, and these are standing agenda discussion items at team meetings.

(c) The need to foster PSAA’s business relationships with suppliers, customers and others

Positive business relationships are recognised to be critical to the company’s future success. Relationships with audit providers are of vital importance. Local audit requires sufficient capacity of specialist knowledge and expertise. Retaining existing suppliers and, if possible, encouraging new firms to enter the market will help to ensure that the market remains sustainable and competitive. Close links and open communications with audited bodies will enable us to understand and better meet their needs. The Board is also committed to building and maintaining strong, effective links with other organisations which perform specialist roles in the new local audit system so that the system as a whole operates efficiently and in a way that meets the needs of audited bodies and users of accounts.

The long-term success of PSAA is therefore critically dependent on the way we work with our customers, suppliers and other stakeholders.

Our customers

Our customers under the appointing person arrangements are opted-in local authorities, police and fire bodies. We operate on a not-for-profit basis, and any surpluses are returned to the audited bodies.

The views of our customers are very important to us and we aim to understand their priorities. We engage with our customers through a variety of different means:

- We have established an Advisory Panel, whose members represent the different types of opted-in bodies. This forum provides helpful feedback and insights into all aspects of our policy making and has enabled PSAA to consult stakeholders and adopt approaches which work for opted-in bodies.

- We ensure that all stakeholders have sufficient time to respond to our consultations, for example, in relation to fees and appointments. Additionally, relevant bodies are consulted in relation to any changes to our new auditor appointments in accordance with PSAA’s governance framework.

- We have established the Local Audit Quality Forum (LAQF) to support the role of audit committees of opted-in bodies in relation to audit quality. Our commitment to audit quality for opted-in bodies features strongly in our monitoring work. We believe that the forum provides a meeting place in which all of the parties that have a responsibility for audit quality can share experiences and good practice. In particular we aim to help local audit committees to play their critical and demanding roles effectively. We hope that audit committee chairs and chief finance officers will be regular attendees and active participants in LAQF events.

- With the LGA and CIPFA we have developed a leaderships essentials training course specifically tailored to meet the needs of audit committee chairs.

- Annually we survey customers as part of our monitoring arrangements in respect of the quality of the services they are receiving. The first survey was conducted in December 2019 and reported in May 2020. The key messages from the survey have been discussed with the audit firms.

- We have attended and presented at a number of local finance, audit and networking group events.

- We will continue to work on enhancing our communications with customers through development of a stakeholder communications strategy as we consider this to be a prerequisite for our continued success.

Our suppliers

Our main suppliers are the audit firms with whom we contract to provide audit services to our customers. The development of strong, long-term relationships with audit firms is not only critical for delivering high quality audit services under the current contract but also for future sustainability of the local audit market.

During the course of audits of the 2018/19 accounts, some of the firms experienced difficulties resourcing all of the audits for which they were responsible on a timely basis to enable audited accounts to be published by the target date of 31 July 2019. The new earlier target deadline for publication has significantly reduced the time available for firms to carry out their post-year end examination of draft accounts leading up to the issue of the final audit opinion. Staff recruitment and retention have proved to be major challenges in the current climate in which the value of audit and the role of auditors is being widely questioned. There is no statutory deadline for the publication of audited accounts but all parties – audited bodies, firms and PSAA – are committed to meeting the 31 July target deadline wherever possible. PSAA is disappointed that these difficulties have arisen and is committed to finding solutions which will avoid similar issues arising in future years. We are very conscious of the disappointment of audited bodies whose audited accounts were not published by 31 July and of the disruptive impact on the work plans of those bodies of rescheduling their audits. We have monitored the position throughout the year and discussed with the firms concerned their recovery plans to complete the audits as soon as possible and to mitigate against a repetition of such problems in subsequent years. However, it is recognised that there are no quick and easy solutions to the issue of scarce auditor resource and implementing any long-term solutions will require all stakeholders to work collaboratively together.

During the year, the Chair and the Chief Executive met regularly with audit suppliers both individually and as a group. This facilitates discussion of issues of common concern, and specifically these meetings have been used as a forum for discussion of the audit resource issue.

To provide transparency and encourage best practice, we publish quality monitoring reports on PSAA’s website on the performance of our contracted firms and the quality of the audits they deliver.

PSAA staff have ongoing communication with firms and audited bodies to agree fee variations. Latest fee variation information is included in the quarterly quality reports that are published on PSAA’s website.

PSAA participates in the groups established to manage the implementation and delivery of the Local Audit and Accountability 2014 (LAAA 2014): The Ministry of Housing, Communities and Local Government (MHCLG) Local Audit Monitoring Board, its local audit sub-group and NAO’s Local Audit Advisory Group. These groups include representatives of the audit firms, the regulatory bodies and government departments.

PSAA staff carry out annual monitoring of each contracted firm addressing both financial health and significant threats to reputation which might be relevant to the firm’s contractual responsibilities to PSAA. The results of this work are reported to the Board by the Chief Executive.

Other key suppliers of services to the company are: the Local Government Association which provide us with our back office services and accommodation; and CIPFA which provide technical reports and publications. PSAA staff meet regularly with these suppliers to ensure positive relationships and early resolution of any concerns.

Wherever feasible, we use the services of smaller suppliers to support the general day to day running of our business.

Other stakeholders

Given our unique position within the local audit environment, we work with a number of key stakeholders and regulators to ensure the quality of local audit services, and we are represented on various key fora.

Our other main stakeholders include MHCLG, the NAO, the FRC, ICAEW, and CIPFA. The Chair and the Chief Executive and/or officers attend meetings with the stakeholders as appropriate, with updates in the Chief Executive’s regular reports to the Board.

We also engage with sector wide initiatives and contribute views and information for Government commissioned reviews and studies. We have contributed to reviews led by Sir John Kingman and the Competition and Markets Authority. During 2019 we have provided information to Sir Tony Redmond and his team for his review of financial reporting and audit in local government as well as responding in detail to his call for evidence. The NAO consulted on their revised Code of Audit Practice for local audit and we responded to both stages of the consultation with a view to securing positive outcomes for audited bodies and users of accounts. In summer/autumn 2020, we will be responding to the NAO’s supporting Auditor Guidance Notes which will provide more detail on the auditor’s responsibilities under the new Code.

(d) The impact of the company’s operations on the community and the environment

The Board regards local audit as an important cornerstone of local accountability. PSAA’s most significant contribution to the community therefore lies in its responsibility to ensure that affordable, high quality audits continue to be delivered to each and every opted-in body by competent suppliers.

The LGA provides a range of support services to the company, including provision of serviced accommodation, HR, ICT and payroll support. As well as operating efficiencies and economies of scale, this arrangement enables PSAA to subscribe to and participate in a range of LGA policies and initiatives. These include flexible/home working, an office recycling scheme, and use of energy efficient office equipment.

PSAA is wholly owned by the Improvement and Development Agency (IDeA) and we have embraced its environmental policy, which includes a commitment to reduce our environmental footprint by:

- continually reducing waste and increasing recycling rate;

- reducing paper use;

- ensuring that procurement of goods and services adheres to the green purchasing and procurement policy; and

- complying with all applicable legislation, regulation and other relevant requirements relating to our environmental impacts.

Our appointing person procurement scheme required suppliers to identify the social value benefits which would accrue from any contract award. This secured commitments to apprenticeships, training and other arrangements which are included in firms’ method statements. Our on-going monitoring of the contract reviews performance against this commitment.

Customers and their local communities will benefit from the significant cost savings realised from our procurement exercise and the re-structuring of PSAA and the related review of our cost base.

The Board annually approves a statement on modern slavery which is published on the website and staff have completed appropriate training.

(e) The desirability of PSAA maintaining a reputation for high standards of business conduct

High standards of corporate governance are a key factor in underpinning the integrity and efficiency of PSAA. We believe that they are critical in helping us to achieve our core objectives as set out in our Articles of Association. During the year we revised our core objectives to reflect the transition of the company to performing the functions of an appointing person. Our arrangements draw on a number of good practice sources including the principles set out in the Code of Conduct for Board Members of Public Bodies (issued by the Cabinet Office) and in the UK Corporate Governance Code, to the extent that the latter can be applied to a small company without shareholders. We review our corporate governance framework annually to ensure it remains fit for purpose and publish full details on our website.

Board Recruitment

Our Chairman is appointed by the IDeA and other non-executive Directors are appointed by the Chairman. The composition of the Board is intended to bring together a range of skills and experience relevant to the governance of the company and its distinctive role and sphere of business. The Board also considers Board succession planning and the leadership needs of PSAA.

Our staff

The company’s structure is designed to ensure PSAA is fit for purpose to fulfil the company’s new appointing person responsibilities. The roles in the new organisational structure are filled by candidates with the necessary skills, qualifications and experience. Most PSAA staff are members of professional accountancy bodies. We encourage and fund staff to attend training and maintain continuing professional development (CPD).

Our stakeholders

We aim to be as transparent as possible about our business, finances, statutory responsibilities and governance including making information available in accordance with the Local Government Transparency Code. From April 2019 PSAA has been subject to the requirements of the Freedom of Information Act. We have developed a policy and staff procedures to ensure that we are compliant with such requirements. PSAA’s publication scheme is on our website and provides detailed information about the company and its functions.

Corporate Governance framework

PSAA has established a robust corporate governance framework which is regularly reviewed. Further details are included in Section 3 of the Strategic Report on Risk Management and within the Governance Report.

The Board is committed to continuing to assess and review its performance and arrangements in relation to the framework now that we have transitioned from a regulatory body exercising powers delegated by the Secretary of State to an organisation operating as a specified appointing person under the Local Audit and Accountability Act 2014.

2. Business review

Auditor appointments

In our fifth full year of business, covered by this report, the company has focused on embedding the arrangements to discharge its appointing person responsibilities.

Appointments have been made for the five years of the appointing period, covering audits of the accounts of opted-in bodies for 2018/19 to 2022/23. Auditor appointments began with effect from 1 April 2018. In order to be eligible for our contracts, firms had to be approved by a relevant recognised supervisory body and five approved suppliers were contracted to provide audit services to opted-in bodies.

| Lot | Firm | PSAA market share |

| 1 | Grant Thornton UK LLP | 40% |

| 2 | Ernst and Young LLP | 30% |

| 3 | Mazars LLP | 18% |

| 4 | BDO LLP | 6% |

| 5 | Deloitte LLP | 6% |

At 31 March 2019 there were 497 local government bodies eligible to opt into the PSAA scheme, 486 (98%) of which had opted in. This high level of support from eligible bodies has enabled us to offer a scheme which maximises benefits and provides excellent value for money for participating bodies.

There have been some minor changes in the number of bodies eligible to opt in. A small number has either ceased to exist or been created (such as new Fire and Rescue Commissioning Authorities). There will be further movement for 2020/21, as various council re-organisations are implemented, and other proposals progress.

2018/19 audits

This year saw delivery of the first audits under the new contract, relating to the 2018/19 financial year. Regrettably, one of the features of the year has been the high number of cases of delayed audit opinions such that at the end of March 2020 there remained nearly 61 opinions still outstanding. The background to these difficulties is outlined in the Overview of the Year at the beginning of this Annual Report.

We have tried to address two of the main concerns bodies have raised about their 2018/19 experience. Firstly, bodies want greater certainty about when their audit will take place and, if for any reason it cannot be undertaken in time to meet the target date for publication of audited accounts, they want to know that is the case at the earliest opportunity. Secondly, if there is any likelihood of additional audit work being required which may lead to a fee variation proposal, again bodies want early information and explanation.

PSAA has worked with auditors to address both of these issues in their audit planning submissions to bodies as part of a concerted effort to strengthen auditor-audited body communications.

Setting audit fees

PSAA’s statutory appointing person responsibilities include specifying a scale or scales of fees for the audit of accounts of opted-in bodies. PSAA is legally required by regulations to set a scale of fees before the start of the financial year to which the fees relate and cannot amend the scale after the start of the relevant financial year. In practical terms, the fee scale must therefore be set more than a year before the relevant audit work is actually started, and before audit work is undertaken under the previous year’s scale fee. This means that for 2020/21 we were required to set the scale fee without complete data for 2018/19 or any data for 2019/20 audits. Additionally, 2020/21 is expected to see the introduction of a series of new developments including revised auditing and accounting standards as well as a new Code of Audit Practice. The impact of these changes is likely to vary between bodies, depending on local circumstances.

We consulted in January and February 2020 on the proposed fee scale for 2020/21. In the absence of any data on the impact of current audit issues on 2019/20 fees, our consultation proposal was to set the fee scale at the same level as 2019/20. In doing so, however, we expect that local auditors will need to engage with individual bodies to discuss the impact of general regulatory pressures and the new developments outlined above on audit fees for 2020/21 and utilise the existing fee variation process, which is subject to our vetting procedures, to reflect the appropriate fee. We recognise that this is likely to lead to additional fees for most if not all bodies.

When we have sufficient information on fee variations, we will be able to establish the extent of additional fees required at each authority where more audit work is needed than is currently provided for in the scale fee.

We welcome all the feedback received to our consultation and thank those who responded. We have published a ‘Q&A’ on our website, setting out the main points from the consultation responses in more detail and providing answers to the particular issues raised. We will update the Q&A periodically to take account of ongoing developments affecting scale fees.

The nature of the challenges facing the local audit environment are such that they do not lend themselves to immediate or easy solutions. Nevertheless, PSAA is committed to work closely with stakeholders to develop solutions and help to build a more resilient sustainable system.

Audit quality

PSAA is also committed to ensuring that its contracted firms provide good quality audits for opted-in bodies. We have developed new arrangements for monitoring audit quality and contract compliance during the five-year appointing period.

We have adopted the International Auditing and Assurance Standards Board’s Framework for Audit Quality (the IAASB framework) as the model for the appointing person audit quality arrangements. Audit quality formed a core part of the evaluation of tenderers in the 2017 audit services procurement, with tenderers encouraged to have regard to the IAASB framework in their responses. Ongoing contract management arrangements have the dual purpose of reporting results to opted-in bodies and ensuring that PSAA meets its obligations under the Local Audit (Appointing Person) Regulations 2015 to monitor compliance of auditors against the requirements in the audit contracts.

Our approach is based on the expectation that a quality audit is likely to be achieved by an engagement team that:

- exhibits appropriate values, ethics and attitudes;

- is sufficiently knowledgeable, skilled and experienced and has sufficient time allocated to perform the audit work;

- applies a rigorous audit process and quality control procedures that comply with law, regulation and applicable standards;

- provides useful and timely reports; and

- interacts appropriately with relevant stakeholders.

While responsibility for providing a quality audit rests ultimately with the auditor, audit quality, efficiency and effectiveness are shared responsibilities. The IAASB framework notes that all parts of the financial reporting supply chain (including audit firms, regulators, standard setters and audit committees) have a role in contributing to and encouraging an audit environment that supports high quality audits. There is a complex interplay of many factors. We have taken the attributes that the IAASB Framework expects to be present within a quality audit and distilled them into three key tests:

- adherence to professional standards and guidance, obtained from the results of professional regulatory reviews;

- compliance with contractual requirements, obtained from monitoring; and

- relationship management obtained from client satisfaction surveys.

The results from the professional regulatory reviews undertaken by the Financial Reporting Council and Institute of Chartered Accountants in England and Wales are not yet available.

We have reported elsewhere on our disappointment that in 208 cases auditors were not able to give an opinion by 31 July 2019 and particularly in those cases where this was caused by insufficient auditor resources. We recognise that audit opinions will also be delayed until such time as the auditor judges they have sufficient assurance to give their opinion.

To coincide with the first audits under the Appointing Person arrangements, we commissioned the LGA Research Team to conduct a survey to obtain audited bodies’ feedback on their audits of 2018/19 accounts. We introduced a new approach incorporating a number of important changes. These changes included a wider scope, confidentiality of responses and independence. The survey arrangements are an important strand of the new Quality Monitoring and Reporting Framework. We have published the results on our website. The survey responses have provided us with the opportunity to identify good practice and discuss specific areas for improvement with individual audit firms.

End of the transitional arrangements

PSAA has been responsible since 1 April 2015 for specific functions delegated to it on a transitional basis by the then Secretary of State for Communities and Local Government. These responsibilities included appointing auditors and setting fees for principal local government and NHS bodies, making arrangements for housing benefits subsidy claim certification, and managing contracts novated to PSAA on the closure of the Audit Commission in March 2015.

The final elements of this work related to the 2017/18 audits of local government bodies. As at March 2020 some of this work is still on-going with 7 audit opinions still outstanding and 34 objections still being investigated. There are also 2 small authority bodies where opinions have not been issued.

During 2019/20 there was a distribution of surplus income, totalling £3.5 million, to relevant audited bodies.

3. Risk Management

Risk management arrangements

The objectives of PSAA’s risk management arrangements are to:

- maintain a risk management framework which provides assurance to the Board that strategic and operational risks are being managed effectively;

- ensure that risk management is an integral part of PSAA’s operations;

- contribute to making informed decisions and effective resource planning; and

- inspire trust and confidence amongst our key stakeholders.

In relation to risk management, the Board is responsible for taking a balanced view of the company’s approach to managing opportunity and risk. The Board’s responsibility includes:

- ensuring that effective arrangements are in place to provide assurance on risk management, governance and internal control;

- ensuring that the risks it faces are dealt with in an appropriate manner, in accordance with relevant aspects of best practice in corporate governance; and

- approving the risk management strategy.

The Board is also responsible for setting the company’s overall corporate risk appetite. As a company responsible for handling public money, PSAA’s tolerance of risk is generally low.

The PSAA audit committee is responsible for reviewing and challenging the company’s assessment and management of risk and the adequacy of internal controls established to manage strategic and operational risks identified. The audit committee scrutinises the corporate risk register at each meeting, and may ask for further reports or presentations on specific risks as it considers necessary. The chair of the audit committee reports to the Board at each meeting on risk management.

The Chief Executive is responsible for maintaining the company’s system of internal control and assurance framework, providing the Board and audit committee with assurance on the system’s ongoing effectiveness and appropriateness, and advising the Board and audit committee as to material changes.

The PSAA team reviews the corporate risk register on a regular basis and specific members of the management team are responsible for managing the individual risks. The team review each of the risks to ensure that the actions identified are up to date/remain appropriate and considers whether there are any new risks that should be added to the risk register.

Current risks

During the year the Board attended a risk management workshop which considered potential risks to the company as it commenced its appointing person responsibilities, moving away from the regulatory role that existed under the transitional arrangements. The exercise resulted in a fully revised and updated corporate risk register designed to identify emerging risks and to ensure that the company’s risk management approach (strategic and corporate risk register) remains fit for purpose.

The significant risks facing PSAA in achieving its business objectives are that:

- Audit firms’ risk/reward assessments of the local audit opportunities conclude that the market is insufficiently attractive leading to a reduction in the number of active suppliers and posing a threat to the competitiveness of the market.

- An audit supplier does not meet PSAA’s contractual requirements in terms of delivery and/or quality.

- PSAA’s scheme and the local audit framework is impacted by Government reviews of the wider audit profession and local audit framework.

- In March 2020 the COVID-19 pandemic meant that social distancing came into effect. This has had a significant impact not only for PSAA but also for our opted in bodies and audit firms. An immediate impact concerns the ability to perform audits and provide audit opinions. This and other repercussions are likely to remain as persistent challenges during 2020/21.

These risks have the potential to impair PSAA’s ability to deliver its functions efficiently and effectively. The audit committee and the Board are sighted in relation to these risks and regularly monitor the arrangements in place to manage them, although recognising that there are significant market factors which are outside of PSAA’s direct control. Where this is the case PSAA actively seeks to work with other stakeholders to influence a sector wide response to the management of risk.

Future risks

Longer term there are a number of wider challenges which have the potential to impact on local audit, audited bodies and PSAA. These include:

- possible changes in audit regulation, auditing standards and audit firms;

- the challenge of ensuring that the local audit system as a whole works effectively and meets the needs of audited bodies and users of accounts;

- the need to maintain a sustainable, competitive local audit market; and

- the related challenge to ensure an adequate supply of suitably qualified and experienced audit staff.

PSAA is seeking to raise the profile of these issues with other stakeholders in the local audit system, and with the review led by Sir Tony Redmond, and is commissioning research and other work to explore options to address these important challenges.

4. Financial review

Being financially responsible

PSAA is committed to securing value for money, ensuring it delivers its objectives while minimising costs. PSAA strives to be financially responsible by:

- exercising financial discipline and maintaining a robust control environment;

- keeping running costs to a minimum;

- returning surplus funds to audited bodies;

- ensuring the company’s internal auditors review the internal control environment annually to provide assurance on the financial controls and confirm these are working as intended;

- meeting the company’s statutory obligations; and

- meeting PSAA’s duties as a good employer.

The company’s internal auditors, TIAA Limited, have reported substantial assurance on all areas reviewed, covering: income flows, the distribution process and a governance review.

Turnover and profit on ordinary activities

The revenue received by PSAA must cover the costs of paying auditors for work under the audit contracts and the operating expenses of PSAA.

PSAA’s accounts show a £nil profit for the 12 months to 31 March 2020 as revenue is matched to expenditure and any monies not required to cover costs are returned to audited bodies.

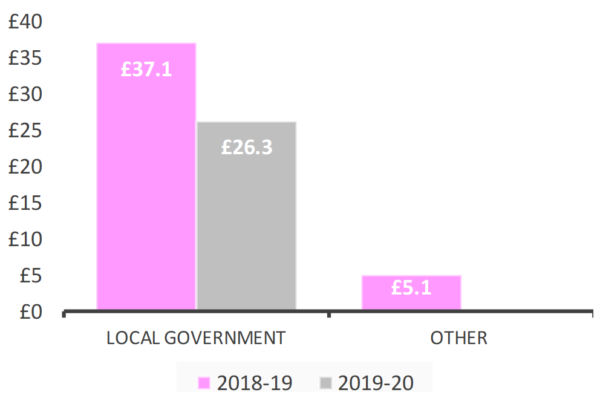

Revenue, including investment income, for the 12 months to 31 March 2020 was £26.304 million (2018/19 £42.214 million) which covered the costs including corporation tax incurred by PSAA for the period 1 April 2019 to 31 March 2020 of £26.304 million (2018/19 £42.214 million).

The reduction in revenue and associated costs is mainly because of the reduction of the scale fees for audit year 2018/19 by 23% and the completion of our responsibilities for grant certification.

Controlling costs

PSAA incurred total costs of £26.304 million, of which the cost of the audit contracts for the period was £25.217 million, 95.9% of total costs (2018/19: £40.612 million which represented 96.2%).

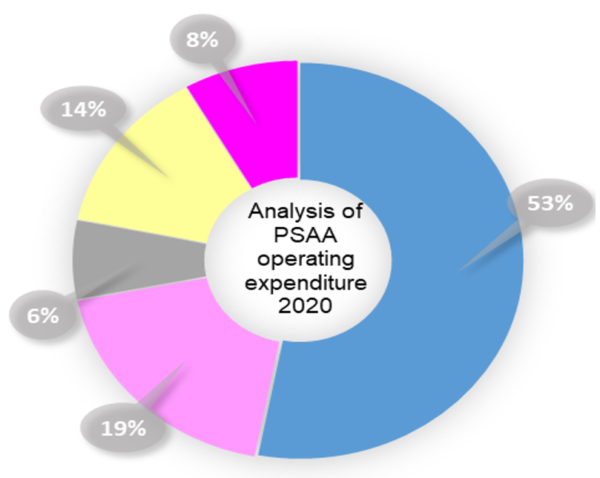

The chart shows the split of PSAA incurred operating expenses of £1.077 million in 2019/20. This represents 4.1% of total costs (2018/19: £1.595 million which represented 3.8% of total costs) and taxation of £0.010 million (2018/19: £0.007 million).

Financial position

PSAA’s total assets equal total liabilities at the end of 31 March 2020 (31 March 2019: total assets also equalled total liabilities). PSAA is required to pay any surplus funds to principal audited bodies, as provided for in its Articles of Association and the Memorandum of Understanding with MHCLG and other parties. Surplus funds are shown as a liability in the balance sheet as part of deferred income. The deferred income is regularly reviewed to ensure PSAA has sufficient funds to pay for its operating expenses and manage its cash flow. Funds no longer required are returned once approved by the Board. At 31 March 2020 the surplus funds remaining were £5.025 million. During 2019 a distribution of the surplus funds under the transitional arrangement of £3.5m was approved by the Board of which £3.3m was paid by 31 March 2020. The remaining amount of £0.2m will be paid in 2020/21.

5. Future developments

The financial year 2020/21 will be a significant one for local audit and PSAA in that:

- Government is likely to make decisions concerning the implementation of some of the recommendations of the reviews of the audit sector (Kingman, Brydon and the Competitions and Market Authority). We will monitor any developments for their potential impact on local audit, the company, opted-in bodies and contracted audit suppliers.

- Similarly, Government is likely to make decisions in relation to recommendations arising from Sir Tony Redmond’s Review and we will again monitor developments in their impact on local audit, the company, opted-in bodies and contracted audit suppliers.

- The revised Code of Audit Practice has passed through Parliament and will be applicable for accounting periods from 2020/21 going forward. The NAO will be consulting on the Auditor Guidance Notes which will set out the auditor’s responsibilities in relation to the new Code of Audit Practice. We will respond to the consultation and consider the impact on the associated fee scale for the remaining three years of the appointing period.

- We will monitor the repercussions of the COVID-19 pandemic on the delivery of audits and signing of audit opinions within the revised timetable set by MHCLG.

By order of the Board

Steve Freer

Chairman

20 July 2020