In our principal and limited assurance regimes, our monitoring of compliance with the Terms of Appointment uses a green, amber, and red scoring scheme.

We also use similar scoring in the principal audit regime to assess the overall quality of audit work for key aspects of the audit covering: financial statements audit work; VFM conclusion; and HB COUNT certification work.

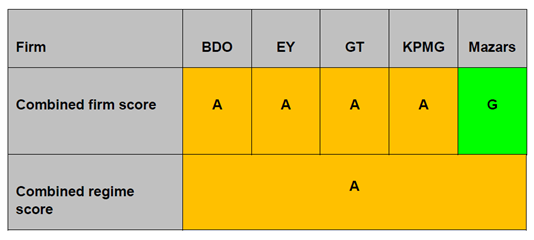

The combined regulatory compliance and audit quality performance for each principal audit firm is detailed in Table 1.

In the limited assurance regime, we assessed whether the work performed by the firms met the required standard.

We were satisfied that:

all firms produced work to an acceptable standard;

all firms met PSAA’s regulatory requirements; and

the risks of failure in the regime were low.

The firms’ individual annual audit quality and regulatory compliance reports, are available to view on the audit quality pages of our website.

Regulatory requirements- principal audits

Our monitoring of auditors’ compliance with the Terms of Appointment focuses on 15 key indicators. These include the target dates for issuing audit opinions on the financial statements and VFM conclusions; reports on the whole of government accounts returns; producing annual audit letters; and sending us specified information and returns.

We are pleased to note that the majority of the indicators were scored as green, where the requirement was either fully met, or met within a specified tolerance.

Auditors met the majority of our target dates for issuing the audit opinion (99.6 per cent for NHS and 94.5 per cent for local government). Where they were not met, the delays were for reasons that were outside the auditor’s control, such as delays at audited bodies in producing financial statements or requiring the resolution of complex objections.

The results of satisfaction surveys issued by firms for 2016/17 audit work showed that audited bodies were satisfied or very satisfied with their auditor.