Overall Performance

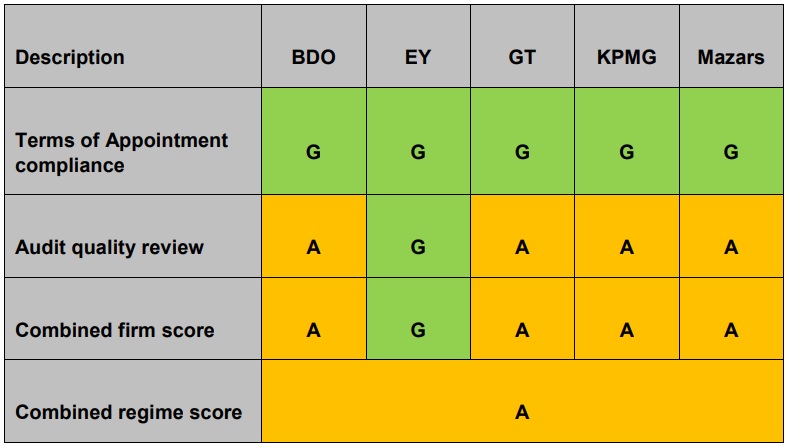

- Table 1 details our analysis of the different elements of our monitoring that underpins our judgement of overall performance. We calculate a red, amber, green (RAG) indicator for each element and component of the QRP (audit quality review and performance requirements). We use a set methodology (detailed in Appendix 1), to produce an overall comparative audit quality rating for each firm and an assessment on the regime as a whole. The audit quality scoring assesses the overall quality of audit work for key aspects of the 2017/18 audit covering financial statements, VFM arrangements conclusion, and HB certification work.

- The results show that all five firms met our overall standards for audit quality and complied with our Terms of Appointment. Whilst improvements were identified as being required there were no reported concerns on the validity of the audit opinions provided.

- The results of satisfaction surveys undertaken by firms for 2017/18 audit work confirmed that audited bodies were generally satisfied or very satisfied with their auditor.

Table 1: Combined Terms of Appointment compliance and audit quality performance scores

- Changes in ratings from year to year reflect a wide range of factors, which may include size, complexity and risk of the individual audits selected for review. Given this and the small sample sizes involved, changes from one year to the next are not necessarily indicative of any overall change in audit quality at a firm. In total four out of 35 financial statement audits were judged as requiring significant improvement by either the AQRT or firms’ internal reviews. This is a reduction of two from the previous year.

- Notwithstanding these results we are concerned that the AQRT and firms’ internal QMRs continue to highlight the same areas of concern as in previous years (addressing the significant risks within Property, Plant and Equipment (PPE) and Pension Fund valuations). Firms need to take action in these areas to improve the consistent overall quality of their audits; the AQRT highlighted that firms’ progression of root cause analysis on these topics has been slow. We recognise that auditors’ judgement on the audit work required to obtain sufficient assurance in respect of local authority PPE and Pension Fund valuations is a matter of significant debate within the sector, and respect the views of the AQRT in defining what is expected in the application of accounting and auditing standards.

- We are also concerned with the timeliness of the QMR process at KPMG where the firm was unable to provide us with the results of one of its reviews for inclusion with in this monitoring report.