The contents of this document will apply from the date of issue until superseded to contracts:

- commencing in April 2023 for the contracts arising from the 2022 audit services procurement.

- for all DPS procurements.

1. Introduction

1.1 These Terms of Appointment and further guidance (the Terms) are issued in accordance with the audit contracts (contracts) between audit firms (Firms) and PSAA. They are effective for all audit appointments made under the Local Audit and Accountability Act 2014 and the Local Audit (Appointing Person) Regulations 2015 (the Regulations). They are issued for the purpose of clarifying the standards for performing the Services under the contracts, and to provide a single point of reference for matters of practice and procedure which are of a recurring nature.

1.2 These Terms will be updated as and when required to ensure they align with changes to legislation, regulations and the Code of Audit Practice (the Code) and following consultation with the Firms, though it is PSAA’s decision as to the changes made.

1.3 Auditors must comply with the requirements set out in the Code issued by the Comptroller and Auditor General (or successor arrangements) in statute, and in the contracts with PSAA.

1.4 The Terms set out service performance standards that auditors must comply with, over and above those set out in legislation, the Code, guidance to auditors provided by the National Audit Office (NAO) and by professional regulators (FRC and ICAEW as Recognised Supervisory Bodies (RSBs)). Nothing in the Terms can override those requirements.

1.5 The Terms form part of the appropriate systems that PSAA, as the specified appointing person, must design and implement under the Regulations to:

- Oversee issues of independence of any auditor which it has appointed, arising both at the time of the appointment and when undertaking work.

- Monitor compliance by a local auditor against the contractual obligations in the audit contract.

- Resolve disputes or complaints from local auditors, opted-in bodies (bodies) and local government electors relating to the audit contracts and the carrying out of audit work by auditors it has appointed.

1.6 Throughout these Terms, the words “Firm” and ‘Auditor’ mean the firm and Key Audit Partners (KAPs) nominated by a Firm to discharge its statutory obligations and its obligations under the contracts. In the event of any conflict, the relevant legislation, the Code and the audit contracts, where applicable, prevail over these Terms.

1.7 Firms must ensure that those working for or on their behalf:

- Comply with the audit services contract (contract) which requires the delivery in accordance with these Terms.

- Are familiar with the PSAA Statement of Responsibilities of Auditors and of Audited Bodies, which outlines the respective responsibilities of the auditor and audited body.

- Have regard to guidance issued by the NAO.

- Refer to PSAA’s published scale of audit fees, which are based on the required audit work.

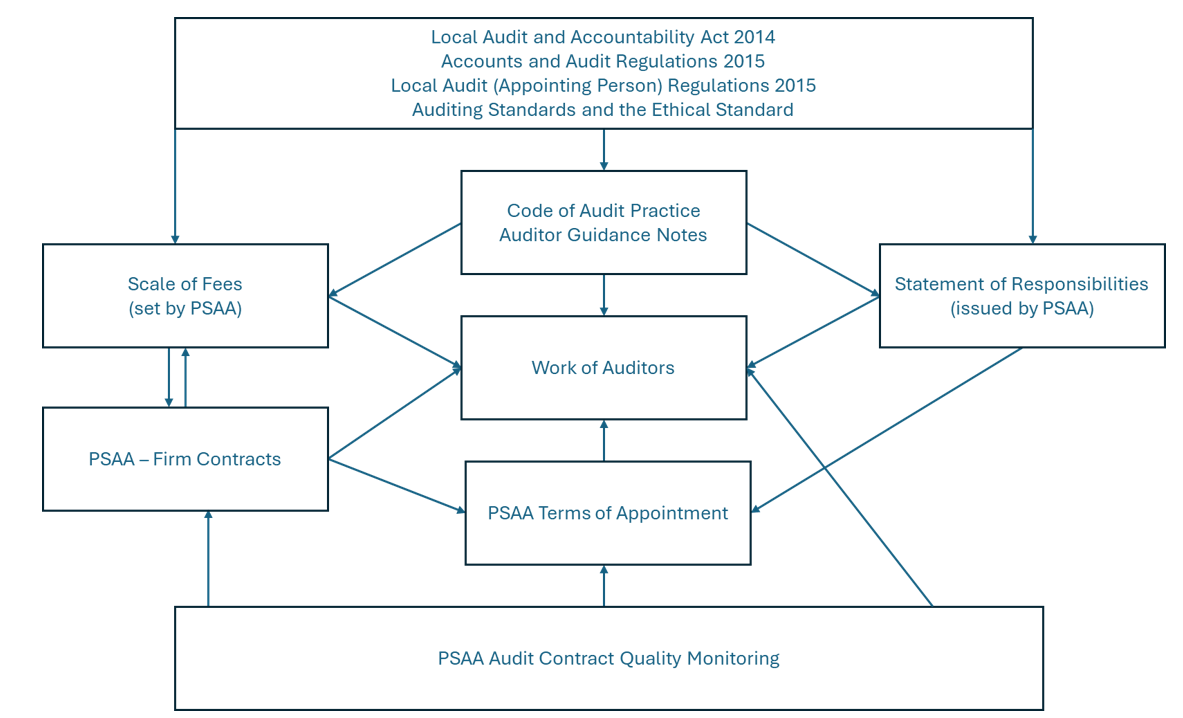

1.8 The diagram below shows how the Terms interact with legislation, the Code, the audit contracts (and other documents) and other guidance produced by the NAO.